The word “crisis” often comes up when talking about journalism in the U.S. and throughout the world: Dropping ad revenue, falling circulation, failed efforts to retool old models to fit a changing media landscape. As the blogosphere and Twitter rise, more opinionated kinds of media coverage push back against the longstanding ideals of impartiality and objectivity, and even the once sacrosanct authority of mainstream journalism is called into question.

But as many journalists, authors and researchers have noted, U.S. journalism has been in transition since its birth, from early broadsides of the revolutionary era through the disruptive entries of radio, television and now the Internet. In his 2012 book, Covering America: A Narrative History of a Nation’s Journalism, author and Boston University journalism professor Christopher B. Daly places the current state of journalism within its recent historical context. Below is an essay based on the book.

————————-

What was it like inside Big Media in the glory days?

Here’s an account from the journalist John Podhoretz, reminiscing about the 1980s:

Time Inc., the parent company of Time, was flush then. Very, very, very flush. So flush that the first week I was there, the World section had a farewell lunch for a writer who was being sent to Paris to serve as bureau chief . . . at Lutèce, the most expensive restaurant in Manhattan, for 50 people. So flush that if you stayed past 8, you could take a limousine home . . . and take it anywhere, including to the Hamptons if you had weekend plans there. So flush that if a writer who lived, say, in suburban Connecticut, stayed late writing his article that week, he could stay in town at a hotel of his choice. So flush that, when I turned in an expense account covering my first month with a $32 charge on it for two books I’d bought for research purposes, my boss closed her office door and told me never to submit a report asking for less than $300 back, because it would make everybody else look bad. So flush that when its editor-in-chief, the late Henry Grunwald, went to visit the facilities of a new publication called TV Cable Week that was based in White Plains, a 40-minute drive from the Time Life Building, he arrived by helicopter — and when he grew bored by the tour, he said to his aide, “Get me my helicopter.”

In the same period, Time was paying its top freelancers in the range of $10 a word (which certainly adds up!). And it was not just Time magazine. At the New York Times, the journalist R. W. “Johnny” Apple Jr. made a reputation not only for his stylish front-page pieces but also for his outlandish expense accounts, brimming with $400 bottles of wine (followed by expensive brandies) and the best rooms at the best hotels. At the Washington Post, the newspaper employed two full-time in-house travel agents just to handle transportation and housing. When reporters needed to go somewhere, they just called the travel desk and let them know. A short while later, a big envelope full of tickets and vouchers would appear. Have a nice trip.

Throughout the 1980s and 1990s, the big media grew much bigger, partly on the strength of their growing audiences, but mainly by taking a page from Wall Street’s book and engaging in the frenzy of mergers and acquisitions that was then sweeping through the rest of the economy. The media consolidation began in earnest in 1985, placing more and more journalism properties inside giant companies that sometimes had little interest in news. That year, Capital Cities Communication (a company previously unheard of in the news media) bought ABC for $3.5 billion, and General Electric bought RCA and its NBC division for $6.3 billion.

In 1986, CBS underwent a friendly takeover by Laurence Tisch and thus passed out of the effective control of William Paley. In 1989, Time Inc., seeking to become too big to take over, merged with Warner Bros. film studios in a record-setting $14 billion deal. The pace quickened again in the mid-1990s. In 1995, CBS changed hands again, bought by Westinghouse for $5.4 billion. The next year brought the purchase of Cap Cities/ABC by Disney Corp. for some $19 billion. In October 1996, Ted Turner took his Turner Broadcasting System into a merger with Time Warner, Inc., creating the biggest media conglomerate to date and combining the newsgathering companies CNN and Time magazine, along with dozens of entertainment properties. In 1999, CBS changed hands yet again when it was bought by Viacom for $37 billion. (It was later spun off and emerged once more as an independent company.) The mentality was simple: grow or die.

Even the giants wanted to get bigger. In 2000, Time Warner merged again, this time teaming up with the Internet phenomenon America Online. Gerald Levin of Time Warner (who never worked as a journalist) was now hitched to Steve Case of AOL (who also never worked as a journalist) in an arrangement that was awkward to begin with and spiraled downhill as AOL began losing money. One casualty of the merger was Ted Turner. When he had brought TBS into the Time Warner fold, Turner solidified his personal fortune, but he was no longer his own boss. Instead, he was given profit targets, just like the heads of other divisions at Time Warner. “For the last four years we were asked to grow 20 percent a year compounded profits for our division. We’ve done it,” Turner said in 2004, but he lamented that the only way to hit those profit targets was to forgo one of his pet projects: hard-hitting documentaries on subjects like the Soviet nuclear program. For a buccaneer with a taste for news, it proved a deal with the devil.

On the day of the AOL–Time Warner merger in 2001, Turner’s personal stake in the combined company was worth more than $7 billion. What none of the principals knew was that the stock price was just about at its peak. In less than three years, Turner’s stake would shrink to less than $2 billion. As more and more Internet users discovered how to browse the Web on their own (especially once Google started helping them), they no longer needed to pay AOL a monthly fee to hold their hand. So AOL stopped growing and began imploding financially, threatening the very existence of the company that Henry Luce had founded in 1923. The Time Warner–AOL merger was shaping up as a case of grow and die.

Growth, but not for journalism

The results of all these corporate mergers and acquisitions was not a net benefit to the practice of journalism. For one thing, most of the deals were, in Wall Street parlance, highly leveraged. That is, the dealmakers used debt rather than cash to buy the properties. As a result, the management was obligated to pay the bankers and bondholders on a relentless schedule. Management issued quarterly profit demands to the heads of divisions for a simple reason: they needed the money. To make matters worse, the stockholders wanted dividends, which also came out of profits, and they wanted to see the value of their shares increase. Under those constraints, big media companies came under tremendous pressure to cut costs and to keep looking for deals that would allow them to borrow even more money to make the company even bigger. The executives who planned and executed these financial maneuvers were not journalists; they were bankers, lawyers, arbitragers, dealmakers. News was not their business; business was their business.

The results of all these corporate mergers and acquisitions was not a net benefit to the practice of journalism. For one thing, most of the deals were, in Wall Street parlance, highly leveraged. That is, the dealmakers used debt rather than cash to buy the properties. As a result, the management was obligated to pay the bankers and bondholders on a relentless schedule. Management issued quarterly profit demands to the heads of divisions for a simple reason: they needed the money. To make matters worse, the stockholders wanted dividends, which also came out of profits, and they wanted to see the value of their shares increase. Under those constraints, big media companies came under tremendous pressure to cut costs and to keep looking for deals that would allow them to borrow even more money to make the company even bigger. The executives who planned and executed these financial maneuvers were not journalists; they were bankers, lawyers, arbitragers, dealmakers. News was not their business; business was their business.

At the same time, there were some notable exceptions. Two important ones in the newspaper business were the New York Times and the Washington Post. Using slightly different techniques, both papers were organized in such a way that the families who owned them exercised effective control over the newspapers at their cores, and both companies were protected from takeovers by outsiders. This meant that the Sulzbergers and the Grahams continued to own (and manage) the two most important daily papers in the country. As long as the money flowed in from circulation and advertising, they could poke a finger in the eye of the federal government, big companies, or almost anyone they thought deserved it. They could maintain costly bureaus in distant places and not have to justify the expense to anyone else. They were not infallible, of course, but they were not subject to corporate overlords, either. The question about both papers at the turn of the century was: How long could it last?

There were other notable exceptions to the corporate takeover of American journalism. Among magazines, several small but important journals of opinion, like The Nation or the New Republic, had patrons with deep pockets who kept them alive for noneconomic reasons. The New Yorker had survived its first few years courtesy of the largesse of Raoul Fleischmann. Then, for decades, it was immensely profitable, right up until 1967, when the number of advertising pages began to drop precipitously. Then followed years of turmoil and turnover, including the sale of the magazine by the Fleischmann family to the privately held Advance Publications, owned by S. I. Newhouse. The New Yorker lost money for eighteen years until it was folded into Condé Nast (a division of Advance Publications) in 1999, and it became modestly profitable again under editor David Remnick while continuing to win prizes and astound readers.

Another major exception to the Wall Street model was National Public Radio, which flourished during these years as a nonprofit. With a growing budget, NPR strengthened its newsgathering capacity, both at home and abroad, and emerged as a major source of news and commentary. The government’s contribution to its budget continued to shrink, as NPR came to rely more and more on sponsors and on “listeners like you.” By 2010 the biggest single source was the voluntary donations from the audience. In addition, another major source of news in America was that venerable cooperative the Associated Press, which supplied a vast amount of hard news (along with sports and business reporting, as well as photos and video) to nearly all of the nation’s news outlets. It remained nonprofit as well.

The most powerful trend in the news business in the late twentieth century was the reorganization of most news outlets into parts of large, publicly traded corporations, often without the ultimate consumers even noticing. In the newspaper field, chains like Gannett, Knight-Ridder, and McClatchy — hardly household names to most readers — gobbled up formerly independent papers. In radio, Clear Channel bought its one thousandth radio station in 2000. Television ownership actually expanded a bit with the arrival of Fox News (a division of News Corp.), but the industry remained one of limited sellers and enormous barriers to entry. The magazine business, too, followed a similar pattern, except that most of the biggest players — Advance Publications (which owns Fairchild Publications as well as the Condé Nast group) and Hearst Corporation — were both privately held companies.

It might be asked: So what? What difference does it make if the news business is, like most of the rest of the economy, in the hands of big corporations? Isn’t the publicly traded corporation the engine that drives the U.S. economy, giving it the dynamism that makes it the envy of the world? It’s a fair question. In the history of the news business, the form of ownership has always mattered, from the colonial print shop through the industrial, family-owned era, to the corporate phase. In the transformation of the news business into a corporate form and then into a conglomerate form, the changes have not been neutral for journalism. The older forms were not perfect — far from it, as the record indicates. But the transformation of traditional media in the late twentieth century also came at a high cost in several respects.

One problem was the drive toward monopoly — or if not monopoly, then what economists call “concentration.” As the number of different owners in any industry shrinks, that industry changes. The survivors face less competition, and they often find it easier as a result to raise prices. If there is a single survivor in the field, then the winner can take all. In the news business, this pattern threatens the very existence of diverse, and local, points of view. Clear Channel replaced more than one thousand individual owners, with different aspirations, different ideas about their civic roles, and different ideologies. The number of U.S. cities with healthy, competing daily newspapers, once in the hundreds, fell to about a dozen. By the year 2000, in American cities that had a daily newspaper, 99 percent had only one management in town. The fifteen biggest newspaper chains account for more than half the nation’s total circulation. In all, there were about 1,500 daily newspapers remaining in America. Of those, only about 350 were independently owned, and most of those were very small. The whole industry was heading in a direction that was at odds with the journalistic values of independence, localism, and competition.

The problem with big

Housing news operations inside such huge conglomerates gave rise to problems. One was the ethical quandary known as conflict of interest. For decades, journalists sought to be independent so that readers and viewers could trust that they were getting the straight dope — about government, about business, even about sports. The idea was that journalists should be able to tell it like it is, without worrying about who benefits or suffers from what their reporting turns up. Independence was the professional ideal. But inside conglomerates, no news operation could be even close to independent. In a notorious example, ABC investigative reporter Brian Ross came across a juicy story. Officials at Disneyworld in Orlando were so hard-pressed to find security guards that they were hiring convicted sex offenders to look after the safety of children visiting the theme park. But his superiors at ABC News decided to sit on the story for fear of offending their own superiors at Disney corporate headquarters. (Those ABC execs had not actually been threatened or told what to do; they were just anticipating the reaction.) All of the paychecks at ABC News come from Disney Corp., so why bite the hand that feeds them? If ABC had still been independent, Ross could have reported his findings and let the chips fall where they may.

Even when there is no pressure (or anticipation of pressure), the ethical problem persists inside big conglomerates. The problem that cannot be eliminated is the appearance of a conflict of interest, which can be just as damaging to an institution’s credibility as an actual conflict. Under parent company GE, for example, every reporter and every editor at NBC News knew that GE made heavy industrial products like jet engines and wind turbines. How aggressive could they have been in looking into problems in those industries? And even if they were professionally aggressive in pursuit of news in those fields, some number of members of the audience were surely aware that NBC’s parent company made those products and would, as a result, have remained suspicious. Or to take another example: the

Washington Post company owns not only the Washington Post newspaper but also Kaplan, Inc., which coaches students on how to pass standardized tests. How aggressive can Post reporters be in evaluating the test-prep business? And even if they do their best, why should readers believe anything they say about Kaplan? Especially since the test-coaching division surpassed the newspaper as the biggest producer of revenue for the parent company. No corporation that includes news and non-news divisions can entirely escape the question of apparent (or structural) conflicts of interest. The problem is inherent in the model.

There are other problems with conglomerate news. While the news divisions may enjoy a measure of independence and First Amendment protections, the likelihood is that some other part of the company is regulated by one or more government agencies. All broadcasters, for example, are regulated by the FCC. Moreover, if the parent company is big enough, there is a likelihood that it sells products or services to the federal or state governments. In that case, how aggressively can the news division be expected to carry out its traditional watchdog role? In fact, most large corporations are inherently unsuited to the practice of journalism. There is an innate caution that is part of the DNA of any large corporation. Large corporations employ large numbers of people — including legions of attorneys, consultants, accountants, and executives (the people known as “the suits”) — who all have perfectly sane and logical reasons for not doing a particular investigation, satire, or routine news story. It is not part of their makeup to go around antagonizing other powerful institutions. Why would a division of GE want to pick a fight with the Pentagon? Why would a company like Westinghouse, which hopes to sell products to the largest possible number of customers worldwide, want one of its divisions, CBS, to investigate an institution like the Catholic Church, or even the Mafia? As a business matter, such an investigation is suicide. But as a journalistic matter, it is essential.

Bad news on the doorstep

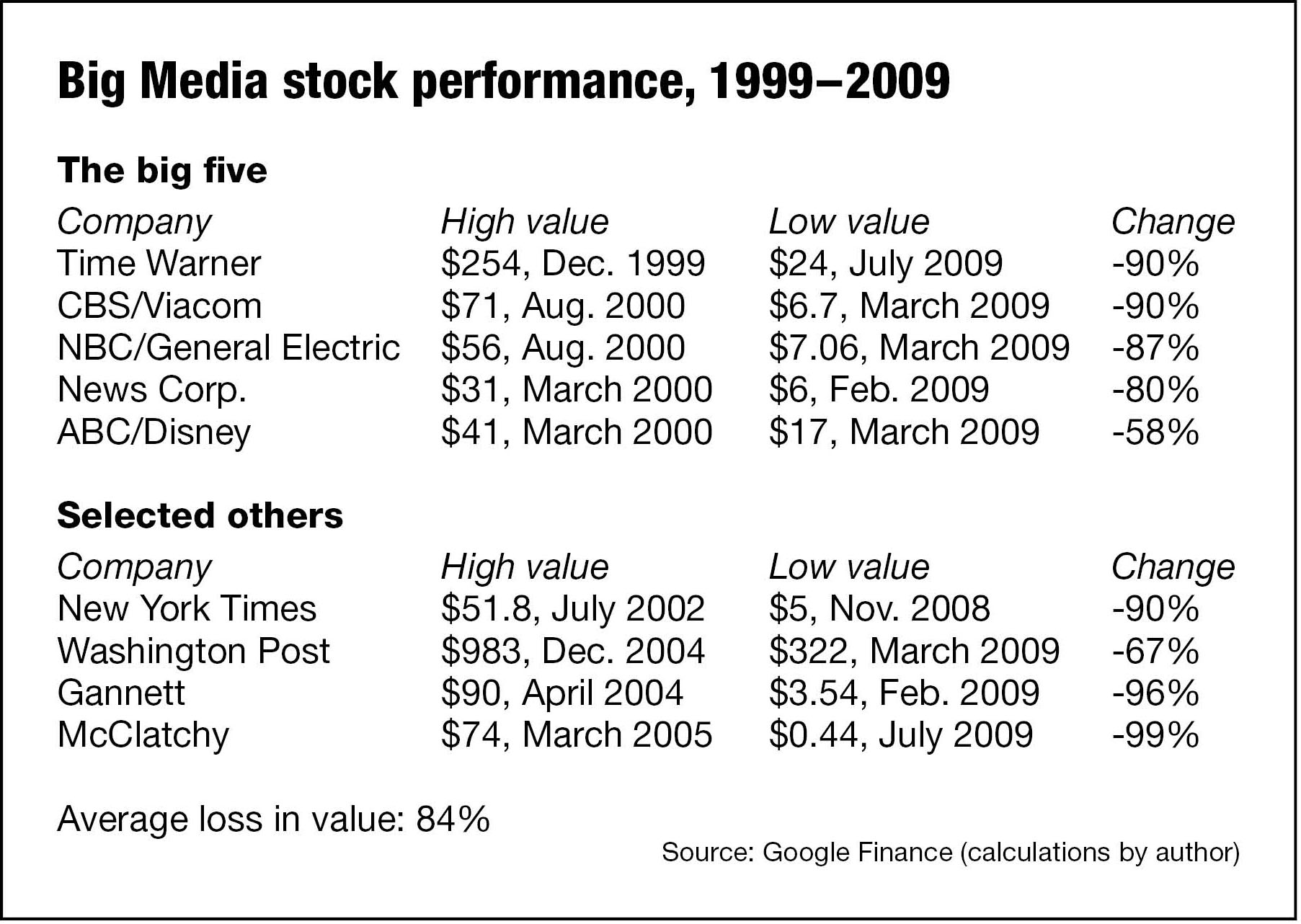

When trouble came, it came fast. Newspapers that measured their lives in centuries, magazines that rounded their circulations to the nearest million, networks that had annual revenues in the billions, all of them thinking that they were on a never-ending upswell of money, power, and sway — all of them went over the cliff together. At the very end of the twentieth century, in December 1999, the value of a share of stock in Time Warner, Inc., one of the mightiest of the Big Five media conglomerates, hit its all-time high: $254 a share. Ten years later it was trading at about $25 a share. In a decade, 90 percent of the value of the company had vaporized. It was not an isolated case.

No sooner had the new millennium arrived than gloom settled over most traditional news media. All of a sudden, revenues were flat or down. Budgets were tighter. Part of the problem was the dot-com economic bust, which was causing the high-flying computer-related companies to slash or eliminate their advertising budgets. Those companies also stopped their initial public offerings of stock, so there were no more of those full-page IPO announcements in the business press. Then came September 11, and suddenly the news mattered again. Americans flipped on their radios and TVs and kept them on. The day after and the day after that, newsstands were sold out of papers. Maybe the news was important after all. Then came the economic aftershock, a mini-recession that made everything even worse. But, the thinking went, maybe this was just temporary and things would turn around. Still, the fact was that the money just wasn’t there. Cuts would have to be made. First came the easy things: expense accounts, part-timers, freelancers, stringers. But those didn’t add up to much. Then came bigger cuts: foreign bureaus, then domestic bureaus, even the Washington bureau. At television news divisions, at the big news-oriented magazines, and at big newspapers, the story was the same.

The economy recovered, but not the news business. By 2004–5 there was a steady drumbeat of cuts, contraction, and worry. Now the cuts were reaching into the heart of most operations, into the newsroom itself. News managers tried to shrink their budgets by offering “buyouts” — in effect, a severance package to pay senior staffers (the ones who were making top pay and who had earned the longest vacations) to go away. When that didn’t solve the problem, the next step was out-and-out layoffs. Many a newsroom became the scene of tearful goodbyes, as security guards watched reporters and editors box up a career’s worth of mementos and junk, then escorted them out of the building. Still, things got worse. In 2008–9 the news was about bankruptcies — the Tribune Company, Philadelphia Media, the Sun-Times Company. Five major newspaper companies filed for bankruptcy between December 2008 and March 2009 and kept publishing while they sought to reorganize their debts. A few newspapers took the ultimate step and closed up shop altogether, or they abandoned print and became available only online. The wolf was not just through the door, it was also devouring institutions that had been decades, even centuries in the making.

The high price of fixed costs

The most endangered of the “legacy” media was also the oldest: the daily newspaper. The problems besetting the typical newspaper by the end of the first decade of the 21st century were many and serious. One was a cost structure that was in part the result of having been in business so long. Like the Big Three automakers, which were also facing extinction at the same time, most large newspapers had enormous “fixed costs.” That is, they were committed to spending a certain large amount of money every day that they did business. Among newspapers at this time, the first fixed cost a publisher faced was the debt incurred in growing to the size of a chain or conglomerate. Just paying the interest on the debt could be crushing. Then there were pensions — legal obligations to keep paying people who hadn’t worked at the paper for years or decades, people hired before the current executives were even born. Those were costs that startups, like all those brand-new news sites and aggregators on the Web, did not face. Plus there were health care costs, and the price of buying health insurance was going through the roof. On top of that there was the payroll, and at most big newspapers that meant union contracts — covering pressmen, drivers, photographers, reporters, you name it — that spelled out how much everyone had to be paid, including overtime in a lot of jobs, and all the vacation, sick leave, and other benefits dreamed up in the good times. To make matters worse, a newspaper company operates what is, in effect, a manufacturing plant. Every day it needs large amounts of raw materials. Tons of paper and buckets of ink have to be fed into enormous presses. Out the other end come hundreds of thousands of objects that have to be placed on a fleet of waiting trucks (no matter how high the price of diesel fuel) and hauled through the crowded streets of the home city, through every suburb round about, and hundreds of miles away to the far reaches of the circulation area. The next day, it all has to happen again.

That kind of operation, with its vast overhead, is utterly dependent on seeing a large and steady stream of revenue coming in to support it all. But in recent years, while most of the costs remained fixed, the revenue went steadily downward. Department stores, once the mainstay of big-city papers, with their full-page ads spreading over multiple pages several days a week, consolidated and stopped competing against one another. In the process, they cut way back on their newspaper advertising. In the classified ad department, long an important profit center at most papers, the phones stopped ringing. The people who needed to sell stuff and the people looking to buy stuff met up on Craigslist or eBay or some other online site and didn’t need the newspaper any more. There went another major source of revenue. Finally, young people mostly stopped reading newspapers — or they stopped reading the print version. Survey after survey showed publishers that the print audience was shrinking and aging. The people in nursing homes were not the demographic that was going to keep the business afloat. But it seemed that almost everyone else was flocking to the Web, where they could get news for free, and letting their subscriptions expire. There went another big revenue source.

Another problem besetting newspapers (and, to a great extent, magazines and television news as well) was even more existential. When seen against the backdrop of the Internet, one fact about newspapers becomes painfully obvious: a newspaper is a fixed bundle of coverage that is good but ultimately second rate. Offering readers no choice, a newspaper presents coverage of a set matrix of topics: politics, crime, business, sports, arts, and something called lifestyle. In each case, though, people who really know or care about those fields understand that they are not going to find the absolute best, most detailed, most passionate coverage of their favorite topic in a daily newspaper. They know that the best coverage will be in some niche on the Web where obsessive amateurs or professional experts gather. And with the coming of the Web, the absolute best coverage is available to everyone, everywhere, all the time, for free. In politics, for example, readers can find pretty good coverage in the Times or Newsweek. But if they really live and breathe politics, they will want it faster and at a much higher level of granularity, so they will log on to a site like Politico or Real Clear Politics instead and get what they are looking for. The same is true for business, sports, even crosswords and recipes. Thus the question arises: What is the remaining value of reading merely pretty good coverage (and paying for it) when readers can unbundle the newspaper, go online, and plunge into first-rate coverage, written by real aficionados and provided at a price of zero?

One way to understand the decline of the newspaper is to ask the ultimate question: If newspapers did not exist, would it make any sense to invent them?

—————–

For a range of personal stories and more recent historical perspective, Stephen Hess’s 2012 book and project for the Brookings Institution, Whatever Happened to the Washington Reporters, 1978-2012, looks at the varied career paths of journalists over more than 30 years. Also of interest is “Riptide,” an oral history of the collision between journalism and digital technology from 1980 to the present. The project is the creation of three Shorenstein Center fellows, John Huey, Martin Nisenholtz and Paul Sagan, who interviewed dozens of people who played important roles in the intersection of media and technology. Huey also sat down and talked to Journalist’s Resource for a research chat earlier this year.

Tags: reporting, news

Expert Commentary