In 2010 the Dodd-Frank Wall Street Reform and Consumer Protection Act was passed, requiring companies to disclose pay differentials in the form of CEO-Employee pay ratios, among various other reforms intended to better inform the American public about the activities of corporations and discourage behavior that could contribute to another financial crisis. Although the legal details of that mandatory disclosure remain in dispute, the pay disparity between CEOs and employees has drawn significant attention from the media and criticism from advocacy groups.

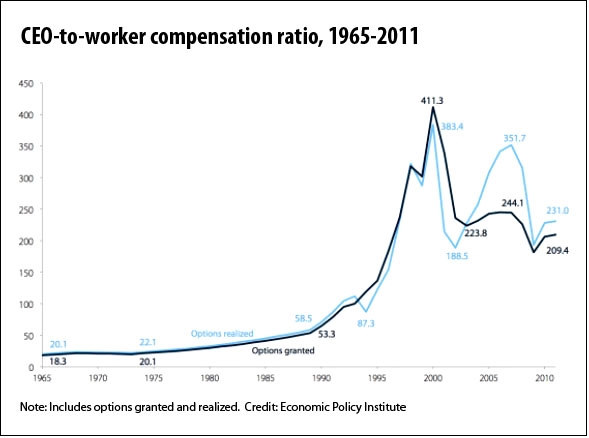

Because executive pay can have a variety of components, there are a number of different methods for calculating this ratio. The Economic Policy Institute notes that “the CEO-to-worker compensation ratio was 18.3 to 1 in 1965, peaked at 411.3 to 1 in 2000, and sits at 209.4 to 1 in 2011.”

In 2013 Bloomberg News estimated the ratio at 204 to 1, up 20% from 2009, across the Standard & Poor’s 500 Index of companies. In 2012, the AFL-CIO estimated the CEO-worker pay ratio to be 357 to 1. There is significant variation across companies, and while some have more modest ratios, some corporations have been called out for having ratios exceeding 500 to 1 or even 700 to 1. (For a look at the salary figures, see the New York Times‘ 2013 chart of the top 200 CEOs.)

Despite the increased attention to the issue, limited research has been done on what determines this disparity or what its effect is on employee motivation and productivity. A 2013 paper by researchers at Northeastern University and Bentley University published in the Journal of Banking and Finance, “The Determinants and Effects of CEO-Employee Pay Ratios,” utilizes data on executive compensation from the Standard and Poor (S&P) ExecuComp database, and on employee compensation from CompuStat. (An open-access version of the paper is available at SSRN.) The authors, Olubunmi Faleye, Ebru Reis and Anand Venkateswaran, examine the relationship between relative pay, measured by the CEO-employee pay ratio, and employee productivity, measured by revenue per employee, taking into account various firm characteristics such as size, performance, board structure and other factors.

The study’s findings include:

- Relative pay of CEOs, measured by the CEO-employee pay ratio, is strongly associated with variables that affect CEO bargaining power, chiefly firm size, performance and risk.

- An increase in one standard deviation in firm size is associated with a 106% increase in the CEO-employee pay ratio. One standard deviation increases in market adjusted stock-return, operating performance, and firm risk, were associated with increases in relative pay of CEOs of 5%, 18% and 12%, respectively.

- Variables related to greater employee bargaining power, such as unionization and greater physical capital intensity, were generally associated with lower relative pay for CEOs.

- An increase of one standard deviation in employee unionization was associated with a 53% decrease in the CEO-employee pay ratio. A similar increase in physical capital intensity was associated with a 24% decrease in this pay ratio.

- In general, the relationship between the CEO-employee pay ratio and firm productivity proves to be statistically insignificant, indicating that relative pay has no impact on the productivity of a firm’s employees.

- Relative pay is significantly and positively related with employee productivity in smaller firms, with a one standard deviation increase in the CEO-employee pay ratio being associated with a 10.5% increase in revenue per employee for firms with fewer than 3,250 employees.

- Firm value increases with higher relative pay for CEOs, with a one standard deviation increase in the CEO-employee pay ratio resulting in a 5.3% increase in firm value. Operating performance is also found to increase with higher relative pay for CEOs.

“These results suggest that observed pay ratios between top executives and ordinary employees arise mainly from the relative ability of workers and executives to negotiate higher compensation with the relevant counterparty,” the authors state. “Workers earn more and pay ratios are lower when ordinary employees enjoy relative strength in negotiating with management, for example, when the workforce is highly skilled or unionized and employees are not easily replaceable.” Furthermore, they find “a positive productivity effect in settings where tournament incentives are plausibly stronger, such as when the firm has fewer employees who are informed on executive pay or are not unionized.”

Keywords: financial crisis, organized labor, CEO pay, inequality

Expert Commentary